A few weeks ago, I was guest speaker during RBC exclusive expert call. Richard Chamberlain and myself discussed about supply chain disruptions and constraints, sustainability, casualization or retail transformation. Last week, Royal Bank of Canada Capital Markets published European General Retail primer; the strong to get stronger, a report that presents latest market trends, financial results, inflation insights, a perspective about ESG, pricing surveys or SWOT analyses.

The following article is a curated selection of insights from the mentioned report:

“Structural trends to reassert themselves. We expect the following structural trends to reassert themselves:

1) A polarisation in performance, with the stronger retailers benefitting from their scale, supplier relationships and pricing power.

2) Omnichannel retailers to gain share, as space reductions ease off and as consumers look for more convenience to suit their more flexible lifestyles.

3) Discounter outperformance – with customers becoming more price conscious and discounters appealing more to middle income shoppers, albeit discounters are likely to face margin pressures.

4) Healthy lifestyles – due to increased consciousness of the benefits of healthy food and living. This is contributing to a still buoyant sports fashion sector.

5) Finally, subject to Covid related restrictions, we see potential for travel and experiential spend to return, with some spend rotation away from Covid winning categories such as home related retail”.

SUPPLY CHAIN DISRUPTIONS

Supply chain disruptions are the new normal. Brexit, climate change and Coronavirus are just a few examples of events that are impacting supply chain. Supply chain constraints seem to be increasing due to economic factors (demand exceeds supply, which I feel is boosting shipping costs, both air and sea freights), and factories in Asia are still not fully re-opened due to covid while some declared bankruptcy). But also, geopolitics (the new geopolitical reality: China vs USA). And then, gas and energy prices are skyrocketing.

In a world of supply chain constraints and product shortages, we think the retailers that are best placed are specialist retailers that a) can offer a broad range, with ample substitutes for lines in short supply b) a relatively high margin (for error) and c) a relatively flexible supply chain.

Where the companies make their money and how they make their money

CLOTHING CONSUMPTION TRENDS AND MARKET SHARES

“China and India should remain the key growth drivers in Asia. Western Europe and the USA remain the largest markets but their growth is slower due to high per capita consumption”.

“In apparel, womenswear is the largest category followed by men’s clothing and footwear. Sportswear and footwear are showing the highest growth rates driven by the ongoing strength in athletic product”.

“The US market is dominated by well-established chains. Off price is more a feature of the market eg TJX is market leader with another discounter, Ross, a prominent player”.

“The Chinese apparel market is very fragmented with Japanese chain Uniqlo prominent but only with just over 1% market share. Following controversies relating to the use of Xinjiang cotton and store closures, both Inditex and especially H&M have lost share in China over the last year”.

MARGIN AND COSTS STRUCTURES

“Retail can be a fairly profitable sector, depending on the level of full price sales. However opex intensity can be fairly high, hence why the market can become fixated on LFL trends.

The table below shows the margin breakdown for retailers under coverage for the last reported fiscal year. We note that some retailers have been heavily impacted by the pandemic, in particular the travel retailers, from whom we expect to see a dramatic margin recovery in the coming years.

In general, from the table, we can see that Currys and M&S are low margin retailers, due to their electricals and food exposure. H&M and Superdry have also had low margins due to the pandemic and some company specific issues. Next and Inditex are both higher margin retailers, with higher gross profit and lower total opex, in a normalised year”.

“We note that margins this year still remain depressed for a number of retailers, as they recover from the pandemic. We note essential retailers (eg B&M) and retailers with more flexible business models (eg Inditex) are likely to have benefitted from the pandemic, and will likely emerge with stronger margins, due to either volume benefits or cost efficiencies made during the pandemic.

We expect the Travel retailers, Dufry and WH Smith, to remain on depressed margins in 2021, given the ongoing weakness in the Travel landscape. We anticipate a more dramatic margin recovery once Travel resumes, likely in 2022-2023″.

Valuation and estimates

Note that the numbers from the table above are in local currencies.

FINANCIAL METRICS FROM INDITEX, H&M, FAST RETAILING AND GAP

Key Financials from leading apparel retailers 2018-2020

Inditex ranked first in 2020 with $24,8 Billion revenues. If COGS margin is around 55% at Inditex (56%), H&M (50%) and Fast Retailing (49%), Inditex is the only one that keeps an EBITDA margin above 20% (EBITDA/Revenues). In 2019, it’s net profit margin (net profit/net sales) was 13%, 5 percentage points higher than Fast Retailing and 7pp higher than H&M.

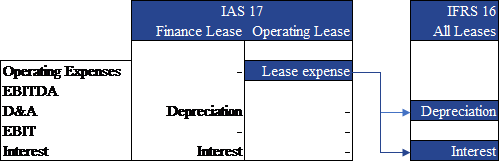

Note that IFRS16 has redefined some financial metrics, specially EBITDA and EBIT. As you know retail uses rentals and leases (e.g. stores rentals). Previous to IFRS16 (a new International Financial Reporting Standard for lease accounting which came into force on 1 January 2019), rentals and leases were classified as operating expenses (OPEX). As you can see in the exhibit 17, rent represents between 10-25% of total OPEX expenses (higher impact in luxury fashion retailers because of their prime location / flasghips store formats).

According to AccountacyAge “The lease expense recognised under IAS 17 will now be recognised as depreciation of the right-of-use asset to be recognised on the balance sheet as well as an interest expense. As a result of implementing IFRS 16, operating expenses will be lower, interest expense will be higher, and EBITDA and EBIT will be higher”. Enterprise software licenses are also considered CAPEX (depending wether it’s on-premise or cloud…).

So, you will need to pay special attention when analysing financial metrics and the enterprise value (EV increases with IFRS 16 as Free Cash Flows and NPV are higher too).

Inditex is showing healthy inventory levels according to sales in such uncertain covid-year while other retailers saw an increase in their inventories compared to their net revenues. This could be a result of a more efficient inventory management enhanced by Inditex omnichannel capabilities (agile supply chain, accurate demand and trend forecasting, RFID, store transfers, ship from store, click & collect, etc).

Inventory % change vs projected sales %

In “Inventory update – who’s running on empty?“, RBC looks looks at inventory positions compared to projected sales in the sector. “This is topical in the light of recent warnings on supply disruptions from the likes of AO World, Gap and Nordstrom. We continue to believe that broadly ranged omnichannel specialists with strong supplier relationships, are best placed to deal with supply disruption.

The level and composition of inventory is a key balance sheet risk item in General Retail, and particularly so at the moment given well documented supply chain bottlenecks. Looking at last reported balance sheet inventory versus projected sales, it looks like Primark and H&M could be short of inventory in some areas, whereas the online fashion retailers could have too much and so may be more at risk of higher than expected markdowns.

More important however is the overall inventory commitment of retailers, rather than the level at the balance sheet date. We think the global fashion retailers eg ITX, H&M and JD/, plus companies with relatively little seasonal risk eg DNLM and SMWH should be best placed to manage through supply shortages. Despite ongoing supply constraints, we see most upside risk to consensus for JD/ and BOSS, while BME to us looks fully valued given tough comps and likely margin headwinds ahead”.

This article is based on RBC latest reports and The Fashion Retailer research.

{kind=link}

This blog is very insightful and perfectly brief out the statistical data delineating pictorial illustrations which really assist me to explore my knowledge further about the vogue brands.